Everyday, Everyday I Have the Blues

By John Stoltzfus,

Chief Investment Strategist

People Get Ready

There’s a new sheriff in town as a new administration takes up the reins in Washington.

With the US presidential inauguration day now behind us, the ECB’s latest rate decision announced last week (they held rates steady), the Federal Reserve’s next FOMC meeting around the corner (less than two weeks away) and with the Chinese New Year and the S&P 500 Q4 earnings season under way, markets stateside and around the world may find an interim period ahead where they become prone to go into a “show me…I’m from Missouri” mode. (For those unfamiliar with that saying, please see the footnote at the end of this commentary.)

For all the skepticism about what’s been coined the “Trump rally” (or even somewhat condescendingly “the Trump Bump”), the markets closed higher on Friday (Inauguration Day) and remain decidedly higher from Election Day November 8th.

As of last Friday from Nov. 8, 2016 (US Election Day): the Dow Jones Industrial Average, S&P 500, NASDAQ Composite, S&P 400 (mid-caps), S&P 600 (small-caps) and Russell 2000 (small-caps) were up respectively 8.15%, 6.16%, 7.20%, 10.73%, 13.98% and 13.11%.

From the end of 2016 into the first three weeks of the new year through last Friday, those same indices have delivered somewhat mixed performances (respective returns of +0.33%, +1.45%, +3.2%, +0.91%, -1.24% and -0.39%), which we’d expect are derived less likely from any lack of confidence among investors in the capability of the US to manage a smooth transition of presidential power or concern about a fiscal stimulus agenda that is still in the planning stage. Most likely markets since the start of the year are reflective of a combination of rotation, rebalancing and some healthy profit taking by tax-sensitive investors.

While there has been no small amount of concern expressed by at least some pundits, commentators, members of the electorate and others about the dramatic change of style of the newly inaugurated president in communicating his message, it appears to us from our vantage point on the Market Strategy Radar Screen (a politically agnostic perch) that there is plenty of interest evidenced by news flow (from sources both pro and against the new administration) in engaging in dialog with the new president.

As market strategists we do not propose to be political strategists. However, having a professional interest in the reaction of the markets to political change (particularly that which could have significant impact on the economy and markets) as well as being practitioners of the discipline of strategic and tactical thinking, we cannot help but consider that much good might come from an agenda that has a stated commitment to effect:

All of the above, if broadly and successfully executed, would appear to us to have a good chance at benefiting workers, businesses, trading partners and our main concerns as investment strategists−investors and the markets.

Like rock n’ roll…it could get loud

In the months ahead we expect the noise level of political dialog and commentary to get loud at times. We do not believe it will be ultimately damaging to the stateside economy, the world economy or the markets.

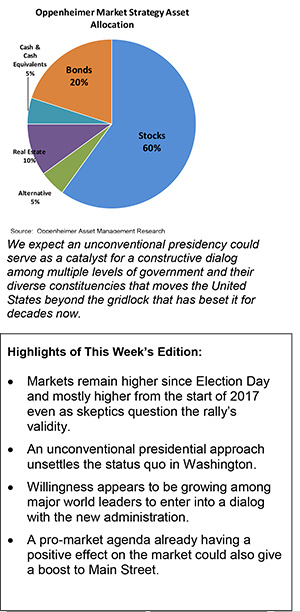

Rather, we expect an unconventional presidency could serve as a catalyst for a constructive dialog among multiple levels of government and their diverse constituencies that moves the United States beyond the gridlock that has beset it for decades now.

Ultimately a distinctive change in approach and style, which has already rattled the establishment, could prove conducive to economic growth, progress and a boost to the standard of living across a broad segment of the population, including current supporters and members of the opposition.

Just over the last week we saw numerous news items that suggest there’s interest expressed from officials in China, the UK, Germany and Mexico to engage in dialog with the new president. Global business leaders less tethered to protocol began the process from as early November 9th.

For the complete report, please contact your Oppenheimer Financial Advisor.

Other Disclosures

This report is issued and approved by Oppenheimer & Co. Inc., a member of all Principal Exchanges, and SIPC. This report is distributed by Oppenheimer & Co. Inc., for informational purposes only, to its institutional and retail investor clients. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. The securities mentioned in this report may not be suitable for all types of investors. This report does not take into account the investment objectives, financial situation or specific needs of any particular client of Oppenheimer & Co. Inc. Recipients should consider this report as only a single factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of the merits and risks of investments. The strategist writing this report is not a person or company with actual, implied or apparent authority to act on behalf of any issuer mentioned in the report. Before making an investment decision with respect to any security discussed in this report, the recipient should consider whether such investment is appropriate given the recipient's particular investment needs, objectives and financial circumstances. We recommend that investors independently evaluate particular investments and strategies, and encourage investors to seek the advice of a financial advisor. Oppenheimer & Co. Inc. will not treat non-client recipients as its clients solely by virtue of their receiving this report. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report. The price of the securities mentioned in this report and the income they produce may fluctuate and/or be adversely affected by exchange rates, and investors may realize losses on investments in such securities, including the loss of investment principal.

Oppenheimer & Co. Inc. accepts no liability for any loss arising from the use of information contained in this report. All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Oppenheimer & Co. Inc. does not represent that any such information, opinion or statistical data is accurate or complete and they should not be relied upon as such. All estimates and opinions expressed herein constitute judgments as of the date of this report and are subject to change without notice. Nothing in this report constitutes legal, accounting or tax advice. Since the levels and bases of taxation can change, any reference in this report to the impact of taxation

INVESTMENT STRATEGY

should not be construed as offering tax advice on the tax consequences of investments. As with any investment having potential tax implications, clients should consult with their own independent tax adviser.

This report may provide addresses of, or contain hyperlinks to, Internet web sites. Oppenheimer & Co. Inc. has not reviewed the linked Internet web site of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the recipient's convenience and information, and the content of linked third party web sites is not in any way incorporated into this document. Recipients who choose to access such third-party web sites or follow such hyperlinks do so at their own risk. The S&P 500 Index is an unmanaged value-weighted index of 500 common stocks that is generally considered representative of the U.S. stock market. The S&P 500 index figures do not reflect any fees, expenses or taxes. This research is distributed in the UK and elsewhere throughout Europe, as third party research by Oppenheimer Europe Ltd, which is authorized and regulated by the Financial Conduct Authority (FCA). This research is for information purposes only and is not to be construed as a solicitation or an offer to purchase or sell investments or related financial instruments. This report is for distribution only to persons who are eligible counterparties or professional clients and is exempt from the general restrictions in section 21 of the Financial Services and Markets Act 2000 on the communication of invitations or inducements to engage in investment activity on the grounds that it is being distributed in the UK only to persons of a kind described in Article 19(5) (Investment Professionals) and 49(2) High Net Worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended). It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. In particular, this material is not for distribution to, and should not be relied upon by, retail clients, as defined under the rules of the FCA. Neither the FCA’s protection rules nor compensation scheme may be applied. This report or any portion hereof may not be reprinted, sold, or redistributed without the written consent of Oppenheimer & Co. Inc. Copyright © Oppenheimer & Co. Inc. 2015.