Everyday, Everyday I Have the Blues

By John Stoltzfus,

Chief Investment Strategist

The Week That Is and the Week That Was

For a second week in a row, the market digests major events.

Monday night brings to the small screen a national, live main event with a broader appeal than most sporting events for an audience hungry for the first of the final series of debates leading to the US presidential election of 2016.

With election night only six weeks and one day away, tonight’s debate is expected by some pundits to draw as many as 100 million viewers (nearly a third of the US population) and almost the size of the Super Bowl audience.

Expectations are high among voters that the evening will both inform and entertain on multiple levels and more importantly shed light and provide specificity as to how the candidates plan to deliver the goods to their respective constituencies and the nation they hope to lead as president and commander in chief.

Investors will be looking beyond the political remarks and jibes for clues as to how the candidates’ respective proposed platforms could affect the stateside economy and even the world economy, as well as what might be the cost burden and budget impact of what is proposed.

Equally important for investors will be the amount of detail provided to add clarity as to what risks and opportunities are likely to develop for the markets from all that is mentioned.

From our perspective as politically agnostic market strategists, we anticipate that this first debate will be well worth the time spent watching it.

Ahead of debate night we revisit our sector views in relation to the candidates with more detail to follow post the first debate.

In last week’s edition of this publication we outlined the sectors that we expected would benefit regardless of which of the two major candidates wins.

Those sector beneficiaries included: Industrials, Materials, Information Technology and Consumer discretionary as both Secretary Clinton and Mr. Trump have highlighted the need for significant fiscal policy to be directed toward infrastructure buildout, replacement and repair.

From what has been heard so far from both candidates it is widely expected that each would be supportive of further government investment in defense, homeland security and cyber security. Each would likely produce programs that would increase spending in these areas that should benefit the previously mentioned sectors as well.

As to health care, pricing (particularly aggressive pricing practices considered egregious) would likely increasingly come under scrutiny and pressure with either a Clinton or Trump administration in the Whitehouse.

Hearings broadcast live from Washington just last week dealing with issues currently emanating from aggressive drug pricing as well as aggressive selling practices at a financial institution likely provided a preview and perhaps the shape of things to come for those sectors (or any sector, for that matter) wherein the operations of a company or a group of companies comes under official scrutiny by elected government officials belonging to either side of the aisle.

That said, we would expect that cyclical and secular drivers will continue to broadly favor those sectors as businesses respond to the needs of their customers, clients and shareholders.

The energy sector as represented by traditional fossil fuel production and distribution would likely benefit under a Trump administration while alternative energy and environmental entities likely would benefit under a Clinton administration.

The Fed’s FOMC meeting press release last week and decision not to raise its benchmark rate did not surprise us, nor did the market’s rally in response to that decision.

While some participants in and around the market were concerned that the Fed’s tone had become more hawkish coming out of the FOMC meeting last week, we did not share that concern.

We have expected for some time this year that the Fed will raise its benchmark rate in December by 25 basis points, if only to remind the markets that the process of rate normalization is ongoing (no matter at how slow a rate) as well as to keep in check any sources of animal spirits or irrational exuberance emanating from the markets.

To us the Fed’s practice of first sending the hawks out over the landscape via previous and current Fedspeak events followed by releasing the doves in subsequent Fedspeak events and commentaries has been an effective method of delivering its message and a format used to manage the process of normalization since Ben Bernanke’s term as Fed chair.

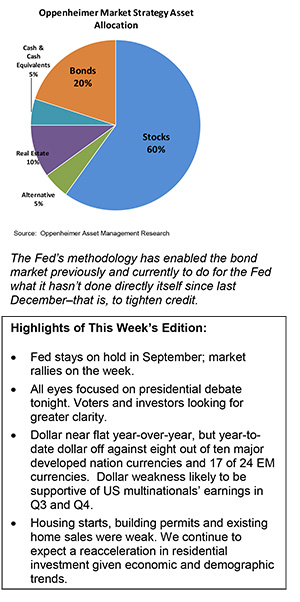

This Fed methodology has enabled the bond market previously and currently to do for the Fed what it hasn’t done directly itself since last December–that is, to tighten credit.

We recall early May of 2013 when then Fed Chair Ben Bernanke announced that the Fed was considering tapering its monthly bond buying program. At the time of his remarks (in early May of 2013) the 10-year Treasury yield was around 1.63%.

After Mr. Bernanke’s remarks, the yield on the 10-year Treasury began to rise, pushed by market forces until it reached a high of 3.02% on December 31st of 2013.

Shortly thereafter the market appeared to recognize that it had inaccurately projected where rates were headed, worries about inflation dispersed and concerns with slowing growth took center stage in the markets. The yield on the 10-year Treasury subsequently dropped, reaching as low as 1.64% in January of 2015.

It’s worth noting that last Friday (September 23, 2016) the 10-year Treasury yield closed at 1.62%. On January 1st of this year the yield on the 10-year stood at 2.27%.

For the complete report, please contact your Oppenheimer Financial Advisor.

Other Disclosures

This report is issued and approved by Oppenheimer & Co. Inc., a member of all Principal Exchanges, and SIPC. This report is distributed by Oppenheimer & Co. Inc., for informational purposes only, to its institutional and retail investor clients. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. The securities mentioned in this report may not be suitable for all types of investors. This report does not take into account the investment objectives, financial situation or specific needs of any particular client of Oppenheimer & Co. Inc. Recipients should consider this report as only a single factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of the merits and risks of investments. The strategist writing this report is not a person or company with actual, implied or apparent authority to act on behalf of any issuer mentioned in the report. Before making an investment decision with respect to any security discussed in this report, the recipient should consider whether such investment is appropriate given the recipient's particular investment needs, objectives and financial circumstances. We recommend that investors independently evaluate particular investments and strategies, and encourage investors to seek the advice of a financial advisor. Oppenheimer & Co. Inc. will not treat non-client recipients as its clients solely by virtue of their receiving this report. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report. The price of the securities mentioned in this report and the income they produce may fluctuate and/or be adversely affected by exchange rates, and investors may realize losses on investments in such securities, including the loss of investment principal.

Oppenheimer & Co. Inc. accepts no liability for any loss arising from the use of information contained in this report. All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Oppenheimer & Co. Inc. does not represent that any such information, opinion or statistical data is accurate or complete and they should not be relied upon as such. All estimates and opinions expressed herein constitute judgments as of the date of this report and are subject to change without notice. Nothing in this report constitutes legal, accounting or tax advice. Since the levels and bases of taxation can change, any reference in this report to the impact of taxation

INVESTMENT STRATEGY

should not be construed as offering tax advice on the tax consequences of investments. As with any investment having potential tax implications, clients should consult with their own independent tax adviser.

This report may provide addresses of, or contain hyperlinks to, Internet web sites. Oppenheimer & Co. Inc. has not reviewed the linked Internet web site of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the recipient's convenience and information, and the content of linked third party web sites is not in any way incorporated into this document. Recipients who choose to access such third-party web sites or follow such hyperlinks do so at their own risk. The S&P 500 Index is an unmanaged value-weighted index of 500 common stocks that is generally considered representative of the U.S. stock market. The S&P 500 index figures do not reflect any fees, expenses or taxes. This research is distributed in the UK and elsewhere throughout Europe, as third party research by Oppenheimer Europe Ltd, which is authorized and regulated by the Financial Conduct Authority (FCA). This research is for information purposes only and is not to be construed as a solicitation or an offer to purchase or sell investments or related financial instruments. This report is for distribution only to persons who are eligible counterparties or professional clients and is exempt from the general restrictions in section 21 of the Financial Services and Markets Act 2000 on the communication of invitations or inducements to engage in investment activity on the grounds that it is being distributed in the UK only to persons of a kind described in Article 19(5) (Investment Professionals) and 49(2) High Net Worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended). It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. In particular, this material is not for distribution to, and should not be relied upon by, retail clients, as defined under the rules of the FCA. Neither the FCA’s protection rules nor compensation scheme may be applied. This report or any portion hereof may not be reprinted, sold, or redistributed without the written consent of Oppenheimer & Co. Inc. Copyright © Oppenheimer & Co. Inc. 2015.