Everyday, Everyday I Have the Blues

By John Stoltzfus,

Chief Investment Strategist

Still Bullish After All These Years

We paraphrase songwriter Paul Simon in anticipation of the 8th anniversary of the bull market which rose like a phoenix from the lows of March 09, 2009.

Even as the market calendar approaches the eighth anniversary of what is so far the second longest running bull market in US history—the week ahead will likely find the attention of investors focused mainly on economic data with a central focus on Friday’s numbers when the Nonfarm Payroll number, the headline US Unemployment rate and Average Hourly earnings cross the proverbial transom.

We’re not surprised that investors’ focus will be on the economic data rather than on preparations to celebrate the market’s anniversary considering that the current Bull Market has been the least loved, the most questioned and the most doubted Bull that we certainly can recall in near 34 years of experience in the markets.

If market tradition were to nickname bull markets the current bull might be appropriately named “the Rodney Dangerfield ‘I don’t get no respect’ market”.

Notwithstanding that likely suitable moniker, we’ve never seen a rising market so prone to constructive self-examination alongside its trajectory evidenced by:

So far throughout the nearly eight years of its tenure, the resilience of the bull market has perplexed its detractors, skeptics and bears worldwide.

It has also been the bull market which in our memory has had consistently over its reign a most powerful ally “riding shotgun” over the US economy—the Federal Reserve—which has provided accommodative monetary policy via extraordinary efforts implemented during and since the crisis of 2008. The effects of the Fed’s efforts are evidenced thus far to have been beneficial to the US economy and the markets stateside.

With the outcome of the recent Presidential election now in the rear view mirror, a business friendlystimulus- focused agenda is in the process of developing its form in the halls of Washington and could appear soon poised to receive the baton to drive growth from the Fed as monetary policy officials move forward with a process of interest rate normalization.

With the US in an apparently sustainable economic expansion based on trends that have developed over the past few years, and an economic recovery that appears more apparent in the international realm from Europe to Asia and elsewhere around the world, investors may find further reason to turn even more positive on stocks.

While Fed funds futures over the course of the past few weeks have moved to levels that signal a progression of from not very likely to highly likely that the Fed would raise rates coming out of the next FOMC meeting on March 15th, this week’s non-farm payroll jobs number, the headline unemployment number and the average hourly wage number will likely be among the deciding factors in what the Fed will do a week from this Wednesday.

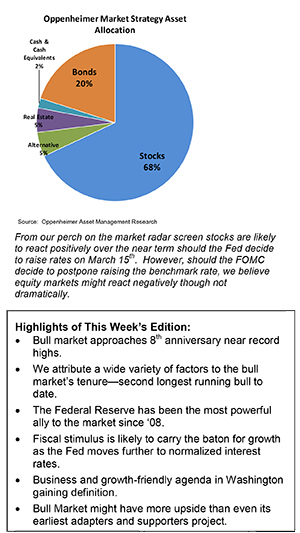

From our perch on the market radar screen stocks are likely to react positively over the near term should the Fed decide to raise rates on March 15th. However, should the FOMC decide to postpone raising the benchmark rate, we believe equity markets might react negatively though not dramatically.

Considering the likelihood for at least two of the three rate hikes for 2017 intimated by Fed Chair Janet Yellen and other Fed officials since December of last year, as well as the underlying support from improving economic fundamentals and likely further improvements in corporate revenue and earnings trends this year, the ever so unloved and disdained Bull Market might have more upside than even its earliest adaptors and supporters project.

For the complete report, please contact your Oppenheimer Financial Advisor.

Other Disclosures

This report is issued and approved by Oppenheimer & Co. Inc., a member of all Principal Exchanges, and SIPC. This report is distributed by Oppenheimer & Co. Inc., for informational purposes only, to its institutional and retail investor clients. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. The securities mentioned in this report may not be suitable for all types of investors. This report does not take into account the investment objectives, financial situation or specific needs of any particular client of Oppenheimer & Co. Inc. Recipients should consider this report as only a single factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of the merits and risks of investments. The strategist writing this report is not a person or company with actual, implied or apparent authority to act on behalf of any issuer mentioned in the report. Before making an investment decision with respect to any security discussed in this report, the recipient should consider whether such investment is appropriate given the recipient's particular investment needs, objectives and financial circumstances. We recommend that investors independently evaluate particular investments and strategies, and encourage investors to seek the advice of a financial advisor. Oppenheimer & Co. Inc. will not treat non-client recipients as its clients solely by virtue of their receiving this report. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report. The price of the securities mentioned in this report and the income they produce may fluctuate and/or be adversely affected by exchange rates, and investors may realize losses on investments in such securities, including the loss of investment principal.

Oppenheimer & Co. Inc. accepts no liability for any loss arising from the use of information contained in this report. All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Oppenheimer & Co. Inc. does not represent that any such information, opinion or statistical data is accurate or complete and they should not be relied upon as such. All estimates and opinions expressed herein constitute judgments as of the date of this report and are subject to change without notice. Nothing in this report constitutes legal, accounting or tax advice. Since the levels and bases of taxation can change, any reference in this report to the impact of taxation

INVESTMENT STRATEGY

should not be construed as offering tax advice on the tax consequences of investments. As with any investment having potential tax implications, clients should consult with their own independent tax adviser.

This report may provide addresses of, or contain hyperlinks to, Internet web sites. Oppenheimer & Co. Inc. has not reviewed the linked Internet web site of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided solely for the recipient's convenience and information, and the content of linked third party web sites is not in any way incorporated into this document. Recipients who choose to access such third-party web sites or follow such hyperlinks do so at their own risk. The S&P 500 Index is an unmanaged value-weighted index of 500 common stocks that is generally considered representative of the U.S. stock market. The S&P 500 index figures do not reflect any fees, expenses or taxes. This research is distributed in the UK and elsewhere throughout Europe, as third party research by Oppenheimer Europe Ltd, which is authorized and regulated by the Financial Conduct Authority (FCA). This research is for information purposes only and is not to be construed as a solicitation or an offer to purchase or sell investments or related financial instruments. This report is for distribution only to persons who are eligible counterparties or professional clients and is exempt from the general restrictions in section 21 of the Financial Services and Markets Act 2000 on the communication of invitations or inducements to engage in investment activity on the grounds that it is being distributed in the UK only to persons of a kind described in Article 19(5) (Investment Professionals) and 49(2) High Net Worth companies, unincorporated associations etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended). It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons. In particular, this material is not for distribution to, and should not be relied upon by, retail clients, as defined under the rules of the FCA. Neither the FCA’s protection rules nor compensation scheme may be applied. This report or any portion hereof may not be reprinted, sold, or redistributed without the written consent of Oppenheimer & Co. Inc. Copyright © Oppenheimer & Co. Inc. 2015.